2020-09-15 / 11월호 지면기사

/ 글|한상민 기자_han@autoelectronics.co.kr

선진국들은 20년 후면 내연기관을 퇴출하고 싶어 한다. 전기차 보급을 더욱 늘리기 위해서는 플러그인 외에도 더 편리한 충전 옵션이 매우 중요하다. 승용차부터 대중교통, 트럭까지 여러 부분에서 무선충전을 포함한 다양한 충전 옵션이 시도되고 있다. 사진은 볼보의 트롤리 충전버스(2017).

Wireless Charging: Beyond EV Branding Hot Item

From the Symbol of Premium to the Urban Mobility Infrastructure

그것이 눈앞에 왔다. 코로나19로 자동차 산업의 일시 후퇴, 무선충전의 미래에 대한 중요한 약속 중 하나인 자율주행 전환이 한쪽(카 메이커의 레벨 3)에서 늦춰지고 있지만, 제동 없는 전기차 전환의 가속과 ‘타도’ 테슬라란 브랜딩 새판짜기가 전기차 무선충전 보급에 청신호를 보내고 있다. 심지어 전기화, 자율주행의 전개 양상이 차량 자체에서 인프라로 관심이 옮겨가면서 무선충전의 시대가 빨라지고 있다.

글|한상민 기자_han@autoelectronics.co.kr

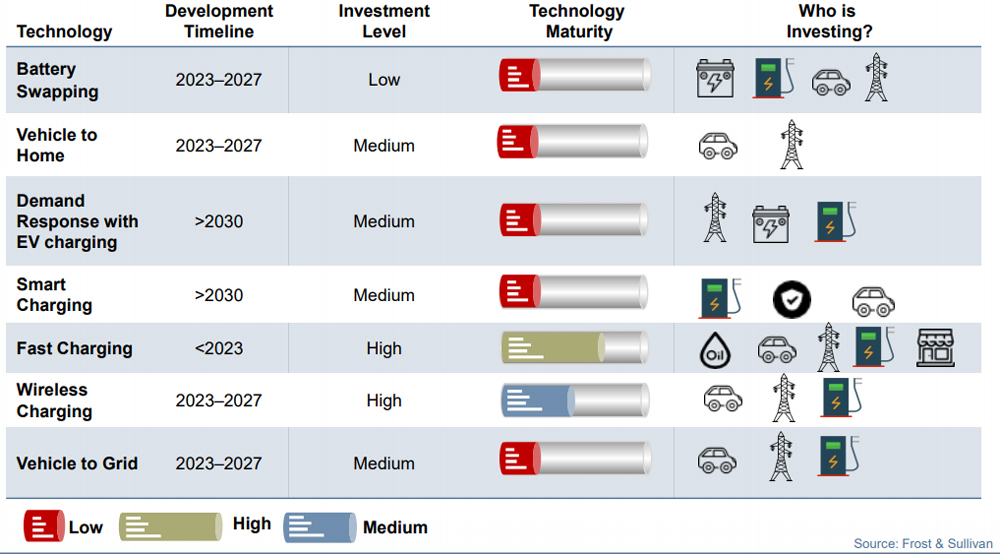

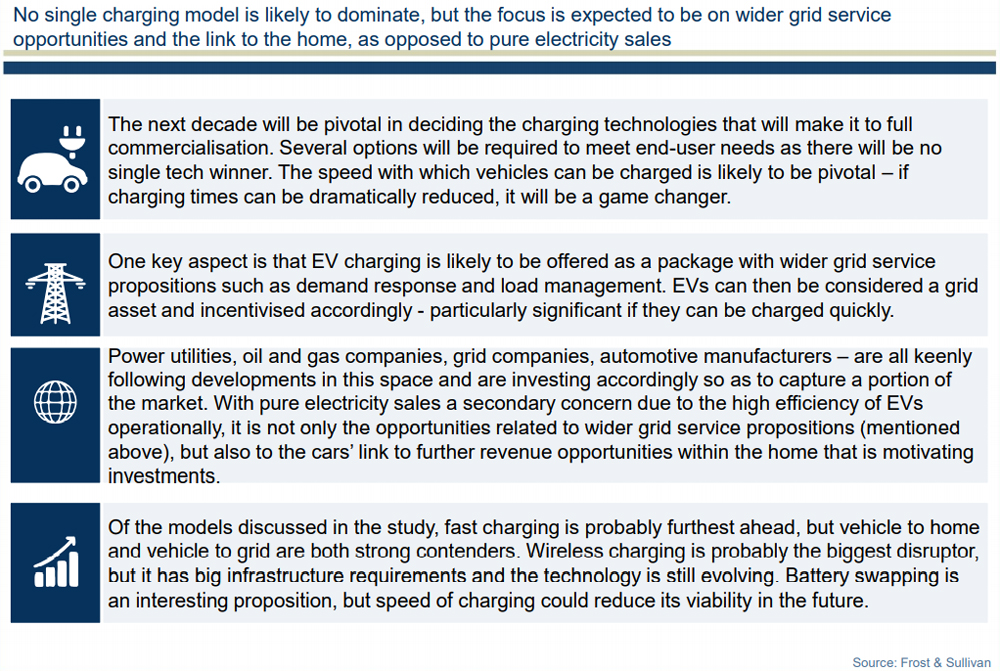

향후 10년간, 전기차 충전 인프라 수요는 승용차, 버스, 트럭, 밴을 포함해 전 세계적으로 사용되는 1억 1,100만 대 이상의 순수 전기차와 플러그인 하이브리드를 통해 일어날 것이다. 이에 따라, 무선충전은 다양한 옵션 중에서도 각광받는 아이템이 될 것으로 예상되고 있다.

현재 무선충전은 전 세계 최대 전기차 생산 및 시장인 중국과 미국, 가장 높은 성장세를 보이는 유럽과 테슬라 따라잡기에 혈안된 독일, 브랜딩 상승을 꾀하는 한국, 첨단의 첨병 일본 등 글로벌 카 메이커의 차세대 승용차를 통해 개화될 조짐을 보이고 있다. 향후 새로운 글로벌 차량 아키텍처의 90%가 무선충전을 지원할 것으로 보인다. 이에 따라 차가 아닌 도시 인프라 차원에서의 무선충전 인스톨 논의도 활발해지기 시작했다.

전기차 충전의 미래 기회와 잠재적 EV 충전 모델 요약, 글로벌, 2019-2030(Frost & Sullivan)

카 메이커 중엔 BMW가 이 부분의 리더로서 양산라인에 적용했다. BMW는 530e iPerformance를 시작으로 2018년부터 옵션으로 제공하기 시작했다. 메르세데스 벤츠의 목표는 새로운 EQ 브랜드에 무선충전을 제공하는 것이다. 폭스바겐 그룹도 무선충전을 전용 전기차 플랫폼에 반영하고 있다. 롤스로이스, 맥라렌과 같은 럭셔리 브랜드는 무선충전 없는 전기차를 상상하지 않는다. 2020년 맥라렌은 스피트테일 슈퍼카에 무선충전을 적용했다. 전기차 전용 브랜드와 프리미엄 제네시스 브랜드의 상승을 꾀하는 현대자동차도 무선충전 적용을 예고했다. 일본의 카 메이커와 티어들도 오래 전부터 무선충전 기술을 내재화하고 론칭을 엿보고 있다.

BMW는 무선충전을 양산라인에 적용했다. 530e iPerformance를 시작으로 고객에게 옵션으로 제공하기 시작했다.

전기차 전용 브랜드와 프리미엄 제네시스 브랜드의 상승을 꾀하는 현대자동차도 무선충전 적용을 예고했다.

전기차 전용 브랜드와 프리미엄 제네시스 브랜드의 상승을 꾀하는 현대자동차도 무선충전 적용을 예고했다.

중국에서

그동안 무선충전 표준의 부재는 비용만큼이나 보급에 큰 장애물이었지만 2년 전부터 빠르게 가시화된 중국의 무선충전 표준 확정은 글로벌 카 메이커의 무선충전 R&D에 기름을 부었다. 전기차 최대 시장 중국의 무선충전 표준 확립은 곧 전 세계 카 메이커의 무선충전 적용을 의미한다.

2020년 5월, 중화인민공화국(SAC) 표준화국이 전기자동차 무선충전 권고기준 4건을 최초로 비준해 발표했다. 이 표준은 중국전기위원회(CEC), 중국자동차기술연구센터(CATRC), 중국전기연구원(CEPRI)이 주관하는 전기자동차 무선충전표준 워킹그룹 내에서 개발됐다. 이러한 중국 GB 표준은 글로벌 표준 기구 중 최초로 비준되고 간행된 표준이다. 이 표준은 2020년 안에 시행될 예정이다.

이와 관련, 미국에 본사를 둔 와이트리시티(WiTricity Corporation)는 무선충전 기술과 지적 재산권의 선도적인 개발업체다. 와이트리시티는 중국, SAE 및 ISO/IEC의 표준화 작업에 중요한 역할을 수행해 왔다. SAE J2954 표준은 2020년 내에, ISO-IEC 표준은 2021년 초에 발표될 것으로 예상된다. 와이트리시티의 특허는 이러한 표준을 구현하는 데 필수적인 것으로 여겨지고 있어, 많은 글로벌 티어 1 공급업체, 인프라 공급업체 및 카 메이커가 라이센스 계약을 맺었다.

예를 들어, 중국의 유력 카 메이커들에게 온보드 차저를 제공하는 티어 1인 VIE(VIE Science & Technology)와 안지 와이어리스 테크놀러지(Anjie) 등은 에너지 전송기술을 포함해 이물질 감지, 위치 감지, 통신 등 요구되는 주변 시스템 모두를 포함하는 와이트리시티의 기술을 라이센스 했다. VIE는 카 메이커 고객을 위한 무선충전 시스템 생산설비를 완료했으며, 안지는 완전 자율주차 및 무선충전 경험을 시연하며 전기 자율주행의 미래상을 보여주고 있다. 글로벌 카 메이커들도 중국에서 플릿 테스트를 진행 중이다.

카 메이커 무선충전 컨셉, 출처|Witricity 홈페이지

그동안 무선충전은 플러그인 충전 생태계와 비교할 수 없을 만큼 침체돼 있었다. 지금은 사라진 에바트랜(Evatran)과 같은 레트로핏 솔루션 회사가 일부 카 메이커와 협력해 애프터마켓을 개척하려고 시도했지만 성공하지 못했다. 이유는 수익성과 타이밍에 민감한 카 메이커들이 무선충전을 애프터마켓 액세서리가 아닌 차량 제조사가 ‘순정부품(original Equipment)’으로 제공해야 하는 기술이라고 생각해왔기 때문이다. 수익성은 물론 보안, 신뢰성 차원에서 카 메이커들은 애프터마켓 공급업체들이 배터리 매니지먼트 시스템 등 전기차의 핵심부를 건드리는 것을 원치 않았다. 게다가 그들은 테슬라나 폭스바겐의 충전사업과 같은 혁신적인 충전 솔루션을 자체 제공하기를 희망한다.

하지만 전기차 시장의 지속적인 폭발, 테슬라의 독주, BMW의 무선충전 상용화, 메르세데스 벤츠, 포르셰 등의 무선충전 적용 예고가 봇물을 이루면서 GB 표준 확정을 전후로 무선충전은 양산 전기차의 필수 기능이 됐다.

와이트리시티에서

이같은 표준 작업의 마무리, 자동차 업계의 실질적인 움직임은 지난해 초 와이트리시티의 무선충전 기술 양대산맥 퀄컴 ‘헤일로(HALO)’ 인수에서 비롯됐다고 볼 수 있다. 당시 퀄컴은 핵심 통신 사업에 집중하기 위해 전기차 무선충전 부문과 모바일 헬스케어 사업부를 매각하기로 결정했다.

결과적으로 와이트리시티는 무선충전 관련 1,500개 이상 특허 및 특허 출원을 싹쓸이했다. 퀄컴과 와이트리시티는 그동안 각각의 레퍼런스 디자인을 글로벌 표준화 기구들이 사용하도록 영향력을 행사하기 위해 경쟁해 왔었다. 양강 구도가 한 가지 버전으로 축소되면서 표준화 및 상호운용성에 대한 진일보가 이뤄졌고 GB 표준 결정에도 결정적 영향을 미쳤다. 와이트리시티는 이제 통합된 특허 포트폴리오에 대한 단일 IP 라이센스를 제공할 수 있다. 지금은 원형 코일 디자인(circular coil design)에 기반한 무선충전용 단일 코일 디자인으로 표준화가 쉬워졌다.

2018, 2019년 와이트리시티는 독일의 유력 티어 1 말레와 중국의 안지, 우리나라의 유라와 같은 굵직한 티어 1과 새로운 라이센스 계약을 체결했다. 우리나라에선 유라에 이어 그린파워가 충전패드 등 무선충전 시스템 구축을 위해 와이트리시티와 라이센스 및 기술이전 계약을 체결했다.

무선충전의 양산차 적용은 비용문제, 설치 공간의 문제(예를 들어 아파트 주차장)로 프리미엄 제품부터 시작된다. 카 메이커들은 이미 어느 정도의 볼륨을 담보할 수 있다면 200~300만 원선에서 고객의 지갑을 열 수 있고, 양산라인 적용이 가능하다고 판단했다. 현재의 무선충전은 경제성을 고려할 때 11 kW급이 대세로 성능 저하 없이 기존 플러그인 충전 방식과 동일한 전력, 효율성, 충전속도를 제공한다.

노르웨이 오슬로는 재규어 랜드로버, 모멘텀 다이나믹스와 함께 2023년을 목표로 세계 최초 전기차 무선충전 택시 승강장 론칭을 추진하고 있다. 75 kW급 급속 무선충전 시스템을 목표로 한다. 버스, 트럭과 같은 EV는 안전, 편의, 빠른 충전 측면에서 더욱 높은 파워의 무선충전이 요구된다.

거리에서

충전은 유선이든 무선이든 충전시간이 길고 불편하기 때문에 차 스스로 하는 것이 미래다. 카 메이커는 무선충전을 단순히 충전에 대한 편리 제공으로만 보지 않는다. 그들이 제공할 발렛 자동주차 기능과 긴밀히 연결된다.

차를 차고 주변에 세우고 자동주차 기능을 통해 주차시킨다고 생각하면 누가 차고로 걸어 들어가 충전 커넥터를 직접 전기차에 물리고 싶겠는가. 또한 COVID-19 대유행 이후 공공장소에서 충전 케이블과 커넥터를 만지는 것은 바람직하지 않을 것이다. 또 공공 주차장에서 로봇암을 이용한 플러그인 자동충전 컨셉의 경우엔 카 메이커의 보안, 신뢰성 측면에서 미래가 불투명해 보인다.

나아가 자율주행 택시나 자율주행 셔틀은 주행거리를 늘리거나 재충전을 위해, 플릿 운영 효율화를 위해 무선충전을 요구할 것이다.

자율주행 모빌리티에서 주차와 자동충전은 서비스 운영의 주요 두 축이다. 자율주행 택시는 누군가의 호출에 따라 스스로 고객을 찾아가 태우고 목적지에 내려주는 것을 반복할 것이고, 차에 운전자가 없기 때문에 충전이 필요할 때 도로 위나 전용 주차장의 충전 패드 위에서 자동 무선충전을 해야 할 것이다. 플러그를 꽂을 지정된 충전소로 돌아갈 때 상당한 양의 에너지를 소모할 수밖에 없다. 때문에 주차장과 대기장소에 설치된 무선충전 포인트를 이용하는 것이 안전하고 에너지가 절감될 것이다.

예를 들어, 내년이면 노르웨이 오슬로에서 전기택시 25대가 충전패드가 내장된 택시 승강장에서 무선으로 재충전할 것이다. 노르웨이는 재규어 랜드로버, 모멘텀 다이나믹스(Momentum Dynamics)와 함께 75 kW급 급속 무선충전 시스템을 시험할 계획이다.

모멘텀 다이나믹스에 따르면, 이 무선충전 시스템은, 예를 들어 버스 아래에 4~6개의 패드를 장착하는데 3만 달러 정도의 비용이 들지만 양산과 함께 1,000달러 이하로 줄이는 것을 목표로 한다. 미국 회사 웨이브(WAVE)와 모멘텀 다이내믹스, 독일 회사 인티스와 IPT 등 전 세계 여러 회사가 버스와 기타 대형 차량을 충전하는 시스템을 개발하고 있다. 이들은 승용차 무선충전 시스템과 유사한 기술을 활용하지만 최대 200 kW의 전력 수준을 처리할 수 있도록 확장된다.

이 밖에도 LEVC 전기 택시를 이용한 프로젝트가 퀼른(TALAKO 프로젝트)에서 전개되고 있다. 올 초엔 영국 정부가 전기택시 무선충전 시험에 340만 파운드 투자를 발표하며 닛산과 LEVC 전기택시 10대를 노팅엄에서 시험할 계획이다. 영국의 스타트업 스프린트 파워(Sprint Power)와 같은 회사가 독일과 영국 전역의 주택가, 주차장, 택시 승강장 등에 무선충전기를 설치하는 프로젝트를 시작했다.

스프린트 파워와 같은 회사는 독일과 영국에서 도시 주택가, 주차장, 택시 승강장 등에 무선충전기를 설치하기 시작했다. 사진은 내용과 관계 없음.

스프린트 파워와 같은 회사는 독일과 영국에서 도시 주택가, 주차장, 택시 승강장 등에 무선충전기를 설치하기 시작했다. 사진은 내용과 관계 없음.

그리드에서

이처럼 대중교통은 점점 더 전기화되고 있고 편리한 충전 인프라를 필요로 하고 있다. 플릿에 대한 충전은 무선충전, 오버헤드 유선충전, 배터리 교환 등 다양한 방식이 있고 전체 충전 인프라의 약 3% 정도만 차지할 것이지만, 고출력 요건과 관련된 추가 비용을 감안하면 미래의 전기차 전체 충전 시장가치의 무려 20% 이상을 차지한다는 점에서 매우 중요하다. 무선충전을 통해 도시교통 차량은 서비스 중에 비 접촉으로 편리하게 충전할 수 있다.

하지만 일반 차량을 위한 충전을 예외로 하면, 대형 차량, 플릿의 경우엔 안전하고 효율적인 충전을 위해 기존 플러그인 충전뿐만 아니라 11 kW급 무선충전으로는 부족하다. 버스와 같은 EV는 대규모 배터리 팩과 무겁고 다루기 힘든 케이블 연결이 필요하며, 특히 충전소는 다른 요소에 개방되어 있고 날씨나 기물 파손에 의해 손상될 수 있어 관리가 어렵고 비용이 많이 들 수 있다. 또 충전시간, 대기시간도 길다. 빠른 충전을 위해서는 파워를 높여야하고, 이렇게 하면 비용은 기하급수적으로 증가한다. 이 비용은 대부분 그리드 업그레이드와 바닥 패드 설치에서 비롯된다.

한편, 무선충전은 V2G(Vehicle-to-Grid)를 가속화할 수 있다. 전기차는 태양열이나 풍력과 같은 신재생에너지원으로부터 에너지를 받아 보다 가치 있게 에너지를 사용할 수 있다. 전력회사는 새로운 에너지 저장 스토리지에 투자하기보다 전기차의 대용량 배터리를 활용하길 원한다. 이것은 양방향 무선충전 기술로 할 수 있다. 단지 충전패드 위에 주차하는 것으로, 플릿은 실시간, 자동으로 전기 값이 쌀 때 충전하고 비쌀 때 되팔아 수익성을 높일 수 있다.

Wireless Charging: Beyond EV Branding Hot Item

From the Symbol of Premium to the Urban Mobility Infrastructure

It has finally come. The auto industry is temporarily retreating due to the covid-19 and the transition to autonomous driving, one of the important promises for the future of wireless charging, is being delayed on one side (level 3 of the car maker). But the acceleration of the electric vehicle conversion and the branding reform called ‘overthrow’ Tesla are sending a green light to the distribution of wireless charging for electric vehicles. The era of wireless charging is accelerating as interest in the development of electrification and autonomous driving shifts from the vehicle itself to the infrastructure(exclusive road).

Over the next decade, demand for electric vehicle charging infrastructure will come from more than 111 million pure electric vehicles and plug-in hybrids used worldwide, including cars, buses, trucks, and vans. Accordingly, wireless charging is expected to become a popular item among various options.

Currently, wireless charging is showing signs of blooming in next-generation passenger cars of global OEM, such as China and the U.S who are world's largest electric vehicle producer and have the world's largest market, Europe who have the highest growth rate, Germany who are struggling to catch up with Tesla, and Korea who are seeking to build a brand value, and Japan who have advanced spearhead tech. 90% of the new global vehicle architecture is expected to support wireless charging in the future. As a result, discussions about installing wireless charging at the level of urban infrastructure rather than cars began to become active.

Among OEMs, BMW applied it to the mass-production line as the leader of this part. BMW began offering the option in 2018, starting with the 530e iPerformance. Mercedes-Benz targets is new EQ brand to offer wireless charging. The Volkswagen Group, has also reflected it on its dedicated electric vehicle platform. Luxury brands like Rolls-Royce and McLaren do not imagine electric cars without wireless charging, and in 2020 McLaren introduced the Speedtail supercar with wireless charging. Hyundai Motor Company, which is seeking to increase the EV-only brand and premium Genesis brand, also forewarned of the application of wireless charging. Japan's OEMs and tier 1 supplier have also internalized wireless charging technology for a long time ago and are looking at the timing of its launching.

In china

Until now, the lack of wireless charging standards has been a major obstacle to dissemination as much as the cost, but the establishment of wireless charging standards in China, which quickly became visible from two years ago, fueled the wireless charging R&D of global OEMs. The establishment of the wireless charging standard in China, the largest electric vehicle market, means that global OEMs will apply wireless charging.

In May 2020, the Standardization Administration of the People’s Republic of China (SAC) ratified and published the first four national China recommended standards for wireless charging of electric vehicles. These standards were developed within the Wireless Charging Standards Working Group for Electric Vehicles administered by the China Electricity Council (CEC), the China Automotive Technology and Research Center (CATARC), and the China Electric Power Research Institute (CEPRI). These China GB Standards are the first to be ratified and published amongst global standards organizations. The standard is planned to become effective within 2020.US based WiTricity Corporation is the leading developer of wireless charging technology and Intellectual Property. WiTricity has played a significant role in the standardization work in China, and the SAE and ISO/IEC. The SAE J2954 Standard s expected to be published within 2020, and ISO-IEC standard in early 2021. WiTricity’s patents are deemed essential to practicing these standards, and have been licensed by many global Tier 1 suppliers, infrastructure suppliers, and OEMs.

For example, Tier 1 VIE(VIE Science & Technology), who provides the onboard chargers to leading Chinese OEMs, and Anjie Wireless Technology (Anjie) have licensed the technology of WiTricity, which in addition to the energy transfer technology includes all the required peripheral systems such as foreign object detection, location detection, and communication, etc. VIE has completed the production facilities for wireless charging systems for OEM customers, and Anjie demonstrates the experience of fully autonomous parking and wireless charging, showing the future of electric autonomous driving. Global OEMs are also conducting fleet tests in China.

Until now, wireless charging has stagnated beyond comparison with the plug-in charging ecosystem. Retrofit solutions companies such as now defunct Evatran tried to workwith some OEMs to pioneer the aftermarket, but were unsuccessful. This is because OEMs, who are sensitive to profitability and timing, have considered wireless charging to be a technology that must be provided as “original equipment” by the carmaker, not as an aftermarket accessory., In terms of profitability, security, and reliability, they do not want aftermarket suppliers to touch the core of the electric vehicle, such as the battery management system. Besides, they hope to offer innovative charging solutions themselves, like Tesla or Volkswagen's charging business. However, with the continuous explosion(rapid growing) of the electric vehicle market, Tesla's far ahead of competitors, BMW's commercialization of wireless charging, and as there are lot of predictions about application of wireless charging by Mercedes-Benz and Porsche, wireless charging has become an essential feature for mass-production electric vehicles around the time the GB standard is confirmed

In WiTricity

The finalization of the standardization work and the actual movement of the auto industry stemmed from the acquisition of Qualcomm's HALO, which is the two major mountains of wireless charging technology, by WiTricity early last year. At that time, Qualcomm chose to sell the electric vehicle wireless charging division and the mobile healthcare division to focus on its core telecom business.

As a result, WiTricity has swept away more than 1,500 patents and patent applications related to wireless charging. Qualcomm and WiTricity had previously been competing to influence global standards organizations to use their respective reference designs. As the two rigid structure has been reduced to one version, further steps have been made in standardization and interoperability, and has a decisive influence on the decision of the GB standard. WiTricity now can provide a single IP license to the combined portfolio of patents. It is now easier to standardize on a single coil design for wireless charging, based on circular coil designs.

In 2018 and 2019 WiTricity signed a new license agreement with Germany's leading Tier 1 Mahle, China's Anjie, and Korea's Yura. In Korea, following Yura, Green Power signed a license agreement and technology transfer contract with WiTricity to build a wireless charging system such as a charging pad.

The application of wireless charging to mass-produced cars starts with premium products due to cost issues and installation space issues (for example, apartment parking lots). OEMs have already determined that if they can secure a certain amount of volume, they can open their customers' wallets at around 2~3 million won and can apply the mass production line. The current wireless charging is 11 kW class in the most popular considering economics, and it provides the same power, efficiency, and charging speed as the existing plug-in charging method without performance degradation.

In street

Regarding charging, whether wired or wireless, charging time is long and inconvenient, so it is the future to do it itself. OEMs don't see wireless charging as simply providing convenience for charging. It is closely linked to the valet automatic parking function they will provide.

If you imagine that you park your car around the garage and park it through the automatic parking function, who will want to walk into the garage and plug the charging connector into the electric vehicle yourself? Furthermore, after the COVID-19 pandemic, handling charging cables and connectors in public settings will be undesirable. In addition, in the case of the concept of plug-in automatic charging using a robot arm in a public parking lot, the future seems uncertain in terms of OEM security and reliability. Furthermore, autonomous taxis and autonomous shuttles will require wireless charging to increase mileage or recharge, and to streamline fleet operations.

In autonomous mobility, parking and automatic charging are the two main pillars of service operation. Autonomous driven taxis will repeat themselves to find customers, pick them up, and drop them off at their destination according to someone's call, and because there is no driver in the car, when charging is needed, it will have to automatically charge wirelessly on the charging pad on the road or in a private parking lot. If they must return to a designated charging station to plug in, they are bound to consume a significant amount of energy. Therefore, they will have to use the points safely built into parking lots and waiting areas.

For example, next year, 25 electric taxis in Oslo, Norway, will be recharged wirelessly at taxi stands with built-in charging pads. Norway intends to test a 75 kW fast wireless charging system with Jaguar Land Rover and Momentum Dynamics. According to Momentum Dynamics, this wireless charging system costs about $30,000 to install four or six pads under the bus but aims to reduce it to less than $1,000 with mass production. Several companies around the world, including US companies WAVE and Momentum Dynamics, and German companies Intis and IPT, are developing systems for charging buses and other large vehicles. They utilize similar technology as the passenger vehicle wireless charging systems, but are scaled up to handle power levels up to 200 kilowatts.

In addition, the project using LEVC electric taxis are being developed in Cologne (TALAKO project). Earlier this year, the British government announced an investment of £3.4 million in wireless charging tests for electric taxi and plans to test 10 LEVC electric taxis with Nissan in Nottingham. Companies such as Sprint Power, British start-up, has begun projects to install wireless chargers in Germany and in residential areas, parking lots and taxi stands across the UK.

From GRID

As such, public transportation is becoming more and more electrified and requires convenient charging infrastructure. There are various ways to charge the fleet, such as wireless charging, overhead wired charging, and battery exchange, and it will only account for about 3% of the total charging infrastructure. But considering the additional cost associated with high power requirements, it is very important in that it accounts for more than 20% of the total charging market value of electric vehicles in the future. Via wireless charging, urban transport vehicles can be charged without sensitive charging dynamics during service.

However, except for charging for general vehicles, for large vehicles and fleets, 11 kW wireless charging as well as conventional plug-in charging for safe and efficient charging is not enough. EV such as buses require large battery packs and heavy and cumbersome cabling, especially charging stations that are open to other elements and can be damaged by weather or vandalism, which can be difficult and expensive to manage. In addition, charging time and standby time are long. It has to increase the input power for fast charging, which increases your cost exponentially. Most of this cost comes from grid upgrades and ground pad installations.

Meanwhile, wireless charging can accelerate V2G. Electric vehicles can use energy more valuable by receiving energy from renewable energy sources such as solar or wind power. Electric Power companies want to utilize the high-capacity batteries of electric vehicles rather than investing in new energy storage. This can be done with bi-directional wireless (V2G, Vehcile-to-Grid) charging technology. Simply parking on a charging pad, the Fleet can increase profitability in real time and automatically by charging when electricity is cheap and discharging (sell to GRID) when it is expensive.

AEM(오토모티브일렉트로닉스매거진)

<저작권자 © AEM. 무단전재 및 재배포 금지>

PDF 원문보기

PDF 원문보기